Business, 10.03.2020 07:57 fraven1819

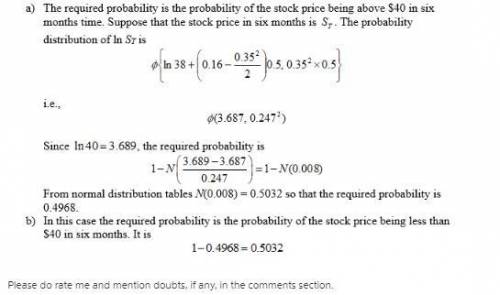

A stock price follows geometric Brownian motion with an expected return of 16% and a volatility of 35%. The current price is $38. a) What is the probability that a European call option on the stock with an exercise price of $40 and a maturity date in six months will be exercised(b) What is the probability that a European put option on the stock with the same exercise price and maturity will be exercised?

Answers: 1

Another question on Business

Business, 22.06.2019 07:00

Imagine you own an established startup with growing profits. you are looking for funding to greatly expand company operations. what method of financing would be best for you?

Answers: 2

Business, 22.06.2019 14:40

In the fall of 2008, aig, the largest insurance company in the world at the time, was at risk of defaulting due to the severity of the global financial crisis. as a result, the u.s. government stepped in to support aig with large capital injections and an ownership stake. how would this affect, if at all, the yield and risk premium on aig corporate debt?

Answers: 3

Business, 22.06.2019 21:40

Which of the following distribution systems offers speed and reliability when emergency supplies are needed overseas? a. railroadsb. airfreightc. truckingd. pipelinese. waterways

Answers: 2

Business, 22.06.2019 21:50

Which of the following best describes the economic effect that results from the government having a budget surplus? a. consumers save more and spend less, enabling long-term financial planning. b. overall demand decreases, reducing the incentive for producers to increase production. c. banks have more deposits, enabling them to make more loans to investors. d. government spending increases, increasing competition for goods and services and driving prices up.

Answers: 3

You know the right answer?

A stock price follows geometric Brownian motion with an expected return of 16% and a volatility of 3...

Questions

Computers and Technology, 01.07.2019 16:10